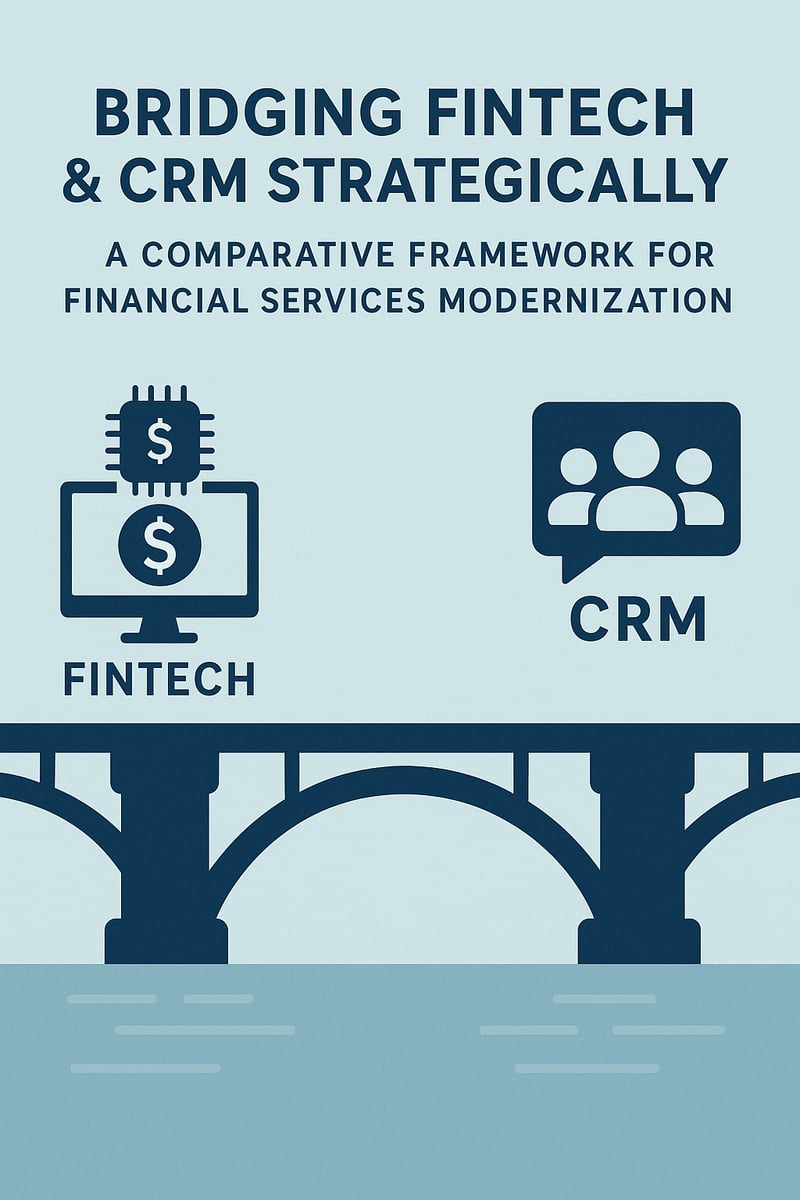

📊 Key Stat: Financial services firms that strategically bridge CRM and FinTech solutions report up to 95%+ identity verification accuracy, phased deployment timelines of 12–24 months, and significantly improved advisor productivity compared to single-platform approaches.

What Are the Strategic Options for Financial Services Modernization?

Financial services firms face three distinct paths when modernizing their technology stack. Understanding the strengths and limitations of each approach is critical to selecting the right strategy for your organization.

What Is the Traditional CRM Modernization Path?

Historically, financial services firms modernized through comprehensive CRM platform upgrades—migrating from legacy systems to modern solutions like Salesforce Financial Services Cloud. Here's how this approach breaks down:

Strengths:

- Unified data model — Supports household-based relationship management across the enterprise

- Proven compliance frameworks — Built directly into the platform for regulatory adherence

- Enterprise-grade scalability — Security and performance at scale

- Rich integration ecosystem — Pre-built integrations and a broad partner network

- Comprehensive support — Robust training and support resources available

Limitations:

- High upfront investment — Licensing, implementation, and change management costs

- Extended timelines — 12–24 months for enterprise deployments

- Customization complexity — Matching unique business processes takes effort

- Adoption challenges — Users may resist comprehensive new platforms

Best For:

- Firms with severely outdated legacy systems creating operational risk

- Organizations seeking to standardize processes across multiple business units

- Institutions prioritizing data governance and compliance centralization

- Companies with scale to justify substantial platform investment

What Is the FinTech Innovation Path?

Alternatively, firms have embraced specialized FinTech solutions—best-of-breed tools for capabilities like portfolio analytics, digital account opening, or AI-powered advice:

Strengths:

- Rapid deployment — Weeks to months vs. years for full CRM platforms

- Superior specialization — Functionality often exceeds generalized CRM capabilities

- Lower initial costs — Subscription-based pricing reduces upfront burden

- Innovation velocity — FinTech vendors rapidly release new features

- Focused UX — User experience designed for specific workflows

Limitations:

- Data fragmentation — Siloed data across multiple point solutions

- Integration burden — Ongoing maintenance as systems and APIs evolve

- Vendor risk — Concentration with specialized, potentially less-established providers

- Compliance complexity — Sensitive data spread across multiple systems

- Hidden costs — Integration maintenance and license accumulation over time

Best For:

- Firms with specific capability gaps requiring immediate solutions

- Organizations comfortable managing multi-vendor technology ecosystems

- Institutions with strong internal IT and integration capabilities

- Companies pursuing differentiation through best-of-breed tool selection

How Does the Strategic Bridge Approach Work?

Leading financial services firms increasingly pursue a third path: strategic bridging of CRM platforms with FinTech innovations. This hybrid approach combines the best of both worlds:

The Model:

- Core CRM platform (e.g., Salesforce FSC) — Serves as system of record and integration hub

- Specialized FinTech tools — Handle capabilities where innovation and differentiation matter most

- Integration layer (e.g., MuleSoft) — Enables seamless data flow and unified user experience

- API-first architecture — Allows modular addition and replacement of capabilities

Strategic Advantages:

- Stability + innovation — Combines CRM reliability with FinTech agility

- Phased modernization — Reduces risk and cost by deploying incrementally

- Safe experimentation — Test new capabilities without wholesale platform change

- Competitive differentiation — Innovate while maintaining operational excellence

This strategic bridge requires thoughtful decision-making about which capabilities to centralize in CRM versus integrate from FinTech solutions—the focus of this guide.

| Approach | Best For | Timeline | Risk Level |

|---|---|---|---|

| CRM Modernization | Enterprise standardization | 12–24 months | Medium |

| FinTech Point Solutions | Targeted capability gaps | Weeks to months | Low (short-term) |

| Strategic Bridge | Long-term competitive advantage | 12–24 months (phased) | Low (incremental) |

How Do You Decide Between CRM Core Capabilities and FinTech Integration?

Not all capabilities should be treated equally in your modernization strategy. Use this four-quadrant framework to assess where to leverage CRM core capabilities versus integrate specialized FinTech:

What Belongs in CRM Core? (High Strategic Value + High Standardization)

These capabilities are foundational to all client interactions, requiring enterprise-wide data consistency and centralized governance:

- Client and household data management — The backbone of relationship management

- Contact and interaction history — Complete timeline of client engagement

- Task and activity tracking — Keep advisors organized and accountable

- Document management — Centralized storage with access controls

- Role-based access control — Security aligned to organizational structure

- Audit trail and compliance reporting — Regulatory-ready record-keeping

Strategic Approach: Leverage native CRM capabilities. Customize within platform boundaries rather than integrating external solutions. Invest in data quality and user training to maximize platform value.

💡 Salesforce FSC Example: Use native Financial Account, Household, and Relationship Group objects rather than building custom objects or integrating external client data management tools. This ensures data consistency, leverages platform security features, and simplifies compliance.

What Warrants Strategic FinTech Integration? (High Strategic Value + Low Standardization)

These capabilities provide competitive differentiation and evolve rapidly with technology innovation:

- AI-powered portfolio optimization — Algorithmic investment strategies

- Predictive analytics — Client behavior modeling and proactive outreach

- Digital advice and robo-advisory — Scalable, personalized recommendations

- Alternative data analysis — Social signals, ESG metrics, and emerging data sources

- Advanced risk modeling — Sophisticated scenario analysis beyond CRM capabilities

- Conversational AI and chatbots — Automated client interaction channels

Strategic Approach: Integrate best-of-breed FinTech solutions while ensuring seamless data flow to/from CRM. Build robust integration patterns enabling flexibility to swap solutions as technology evolves.

Implementation Pattern: Connect AI-powered advice engine to Salesforce FSC via MuleSoft. Client profile data flows from FSC to the advice engine; personalized recommendations flow back and surface in the advisor console. The advisor can accept, modify, or reject recommendations—all tracked in CRM.

What Are Commodity FinTech Integrations? (Low Strategic Value + Low Standardization)

These tools support operational efficiency rather than differentiation and are widely available from multiple vendors:

- E-signature tools — DocuSign, Adobe Sign

- Video conferencing — Zoom, MS Teams

- Calendar scheduling — Calendly, Microsoft Bookings

- Standard payment processing — Routine transaction handling

- Basic document generation — Templates and automated documents

Strategic Approach: Select solutions based on cost, ease of integration, and user familiarity. Avoid over-engineering integrations—simple data pass-through is often sufficient. Be prepared to switch providers if better options emerge.

Implementation Pattern: Embed DocuSign flows in Salesforce FSC using pre-built connectors. Trigger document generation from CRM workflows, track completion status, and store signed documents in Salesforce Files. Avoid deep customization to allow easy migration to alternatives if needed.

When Should You Use CRM or Low-Cost Integration? (Low Strategic Value + High Standardization)

These capabilities are required but not differentiating. They benefit from standardization but don't drive strategy:

- Basic marketing automation — Email campaigns, lead capture

- Standard reporting and dashboards — Operational performance views

- Simple workflow automation — Rule-based process automation

- Contact enrichment and data hygiene — Maintaining clean records

- Basic mobile access — On-the-go CRM functionality

Strategic Approach: Use CRM native capabilities when "good enough." If specialized tools are required, integrate low-cost solutions and avoid over-customization. Focus implementation effort on higher-value quadrants.

💡 Salesforce FSC Example: Use Marketing Cloud Account Engagement (Pardot) for standard lead nurture rather than integrating expensive specialized marketing automation. For most financial services firms, sophisticated marketing automation doesn't drive competitive advantage—focus innovation investment elsewhere.

Should You Build, Buy, or Bridge? Real-World Scenario Comparisons

How Do CRM, FinTech, and Bridge Approaches Compare for Client Onboarding?

Client onboarding and KYC is one of the most impactful areas to evaluate your modernization strategy. Here's how each approach compares:

Traditional CRM Approach:

- Build custom onboarding flows in Salesforce using Process Builder/Flow

- Store documents in Salesforce Files

- Manually track KYC status and expiration dates

- Use validation rules to enforce data completeness

FinTech Point Solution:

- Implement specialized onboarding platform (e.g., Alloy, Onfido)

- Leverage advanced identity verification and document analysis

- Automated risk scoring and decision-making

- Real-time integration with credit bureaus and sanctions lists

Strategic Bridge Solution:

- Use Salesforce FSC for client data management and relationship tracking

- Integrate specialized KYC/onboarding FinTech for identity verification

- Flow: Client data passes from FSC to FinTech → verification and risk scoring → results return to FSC

- Advisor sees unified view in Salesforce with KYC status, document access, and next steps

| Dimension | CRM Only | FinTech Only | Strategic Bridge |

|---|---|---|---|

| Time to Deploy | 3–4 months | 2–3 months | 4–5 months |

| Upfront Cost | $50K–$75K | $30K–$50K | $80K–$120K |

| Annual Ongoing | $10K–$15K | $25K–$40K | $30K–$45K |

| ID Verification Quality | Basic (65–70% accuracy) | Advanced (95%+ accuracy) | Advanced (95%+ accuracy) |

| Advisor Experience | Native, no context switching | Separate login/system | Unified within CRM |

| Compliance Audit Trail | Complete | Fragmented | Complete |

| Flexibility to Change | Moderate | Low (vendor lock-in) | High (modular) |

Recommendation: Strategic bridge approach for firms with >$1B AUM or strong compliance requirements. Pure FinTech for fast-growing startups prioritizing speed over integration. CRM-only for firms with basic needs and limited budget.

Which Approach Works Best for Portfolio Analytics and Reporting?

Traditional CRM Approach:

- Use Salesforce CRM Analytics (Tableau CRM) for dashboards

- Import position data from custodians via scheduled jobs

- Build custom reports for client statements

- Limited analytics beyond basic aggregations

FinTech Point Solution:

- Implement specialized portfolio analytics platform (e.g., Addepar, Black Diamond)

- Real-time position data and performance calculation

- Sophisticated risk analytics and scenario modeling

- Institutional-grade reporting and client portals

Strategic Bridge Solution:

- Use FinTech platform as portfolio analytics engine

- Surface key metrics and visualizations within Salesforce FSC

- Maintain full portfolio detail in specialized system

- Enable deep-dive from CRM to analytics platform when needed

| Dimension | CRM Only | FinTech Only | Strategic Bridge |

|---|---|---|---|

| Analytics Sophistication | Basic aggregations | Institutional-grade | Institutional-grade |

| Real-time Data | Batch updates (daily) | Real-time | Near real-time |

| Advisor Workflow | Context switching for details | All in analytics platform | High-level in CRM, detail on-demand |

| Client Portal Quality | Basic | Sophisticated | Sophisticated |

| Total Cost (3 years) | $150K–$200K | $300K–$500K | $350K–$550K |

| Scalability | Limited beyond 10K accounts | Scales to millions | Scales to millions |

Recommendation: Strategic bridge or pure FinTech for wealth managers with sophisticated analytics needs. CRM-only for insurance agencies or banking with limited investment management.

What Is the Best Strategy for Marketing Automation in Financial Services?

Traditional CRM Approach:

- Use Salesforce Marketing Cloud or Pardot

- Email campaigns triggered from CRM data

- Landing pages and forms feeding lead records

- Standard nurture campaigns and drip sequences

FinTech Point Solution:

- Implement specialized financial services marketing automation (e.g., Snappy Kraken, FMG Suite)

- Pre-built campaigns and content for financial topics

- Compliance-reviewed templates and workflows

- Integrated social media and video marketing

Strategic Bridge Solution:

- Use FinTech platform for campaign creation and content management

- Sync campaign engagement data to Salesforce FSC

- Trigger campaigns from CRM events (account milestones, life events)

- Maintain contact management and segmentation in CRM

| Dimension | CRM Only | FinTech Only | Strategic Bridge |

|---|---|---|---|

| Content Quality | Generic, requires customization | Financial services-specific | Financial services-specific |

| Compliance Review | Manual process required | Pre-reviewed by vendor | Pre-reviewed by vendor |

| Campaign Setup Time | 2–3 weeks per campaign | Days per campaign | Days per campaign |

| CRM Data Utilization | Full integration | Limited, manual exports | Automated integration |

| Total Cost (Annual) | $36K–$60K | $24K–$48K | $48K–$72K |

| Advisor Adoption | High (familiar interface) | Moderate (new platform) | High (managed from CRM) |

Recommendation: Strategic bridge for firms prioritizing advisor experience and data-driven segmentation. Pure FinTech for smaller firms (<50 advisors) seeking quick wins. CRM-only for enterprises with marketing teams capable of building financial content.

How Should You Sequence Your FinTech-CRM Modernization Journey?

What Does a Phase-Based Approach to Strategic Bridging Look Like?

A successful modernization follows four distinct phases over 24 months:

Phase 1: Stabilize the Core (Months 0–6)

- Deploy or upgrade core CRM platform — Salesforce FSC as the foundation

- Migrate foundational data — Clients, households, accounts

- Establish data governance — Security model and data quality standards

- Train users — Core CRM capabilities and workflows

- Goal: Create a stable foundation for future integration

Phase 2: Integrate Strategic Differentiators (Months 7–12)

- Identify 2–3 high-impact FinTech integrations — Quadrant 2 from the framework

- Implement integration layer — MuleSoft if not already present

- Deploy initial FinTech connections — With robust error handling

- Measure business impact — Refine based on usage data

- Goal: Demonstrate quick wins from strategic bridging

Phase 3: Optimize Operations (Months 13–18)

- Add commodity integrations — Quadrant 3 tools to reduce friction

- Automate cross-system workflows — Spanning CRM and FinTech systems

- Enhance user experience — Embedded FinTech capabilities in CRM

- Scale across business units — Roll out successful integrations firm-wide

- Goal: Drive operational efficiency and user adoption

Phase 4: Innovate and Differentiate (Months 19–24)

- Experiment with emerging capabilities — AI, blockchain, advanced analytics

- Replace underperformers — Swap out integrations that aren't delivering

- Develop proprietary models — Leverage integrated data for unique insights

- Establish center of excellence — Ongoing innovation governance

- Goal: Create sustainable competitive advantage

What Are the Most Common FinTech-CRM Integration Mistakes?

Avoid these four critical mistakes that derail modernization efforts:

| Mistake | Why It Happens | How to Avoid It |

|---|---|---|

| Integrating before core stabilization | Pressure for quick wins | Ensure data model, security, and basic workflows are stable first |

| Too many simultaneous integrations | Over-ambitious roadmaps | Limit concurrent integrations to 2–3 at a time |

| Neglecting the integration layer | Cost-cutting on infrastructure | Invest in MuleSoft or similar middleware early to avoid spaghetti architecture |

| Treating integration as one-time | Project vs. product mindset | Budget for ongoing maintenance as FinTech APIs evolve continuously |

How Do You Assess Your Organization's Integration Readiness?

Evaluate your organization's readiness for strategic bridging across five weighted dimensions:

What Are the 5 Dimensions of Integration Readiness?

1. Technical Capability (Weight: 30%)

- Enterprise IT architecture expertise — Does your team understand modern integration patterns?

- API development and management — Can you build, document, and maintain APIs?

- Security and compliance knowledge — Can you assess and mitigate integration security risks?

- DevOps and monitoring — Can you support 24/7 monitoring and incident response?

2. Organizational Change Capacity (Weight: 25%)

- Executive sponsorship strength — Clear commitment from C-suite?

- User adoption track record — Historical success with technology changes?

- Training infrastructure — Established processes for user enablement?

- Change champion network — Power users who evangelize new tools?

3. Financial Resources (Weight: 20%)

- Upfront capital availability — Can you fund platform and integration investment?

- Ongoing operational budget — Sufficient resources for annual maintenance and enhancement?

- Opportunity cost tolerance — Can you absorb implementation impact on current operations?

- ROI patience — Willing to wait 12–24 months for full benefits?

4. Data Quality and Governance (Weight: 15%)

- Current data accuracy — How clean is your existing client/account data?

- Data governance processes — Established rules for data entry and maintenance?

- Master data management — Clear system of record for each data domain?

- Data integration experience — History of successful data migrations and synchronization?

5. Competitive Urgency (Weight: 10%)

- Market pressure — Are competitors outpacing you with technology?

- Client expectations — Are you losing business due to technology gaps?

- Regulatory drivers — Do compliance requirements necessitate change?

- Strategic imperatives — Is modernization critical to business model evolution?

How Should You Interpret Your Readiness Score?

| Score Range | Strategy | Timeline | Key Actions |

|---|---|---|---|

| 80–100 | Aggressive Strategic Bridge | 12–18 months | Full FSC + MuleSoft + 2–3 FinTech integrations in parallel |

| 50–79 | Measured Strategic Bridge | 18–24 months | Core CRM first, then 1–2 high-impact integrations sequentially |

| 20–49 | Stabilize Then Integrate | 24–36 months | Focus on CRM deployment, data quality, and one low-risk FinTech integration |

| <20 | Partner-Led Modernization | 36+ months | Engage experienced partner, CRM-only first, build internal capability |

What Makes Vantage Point's Integration Methodology Different?

Vantage Point's approach to strategic bridging is grounded in two decades of financial services technology experience. We don't believe in one-size-fits-all solutions. Instead, we conduct comprehensive capability assessments, develop tailored integration strategies, and deliver implementations that balance innovation with operational excellence.

What Is Vantage Point's Distinctive Approach?

- Business-First Technology Strategy — We start with business outcomes, not technology features. Our integration strategies deliver measurable improvements in advisor productivity, client experience, and operational efficiency—not just elegant technical architectures.

- Risk-Calibrated Implementation — Financial services firms can't afford disruption to client service or compliance failures. Our phased approach validates each integration thoroughly before proceeding, with rollback plans and business continuity measures at every stage.

- Build-Operate-Transfer Model — We don't just implement and walk away. Our managed services team operates your integrated environment during stabilization, proactively resolving issues before they impact users. As your internal team gains proficiency, we transfer operations knowledge systematically.

- Future-Proof Architecture — We design for change. Our integration patterns are modular and well-documented, enabling you to swap FinTech components as better solutions emerge. You're never locked into today's choices.

What Are the Key Takeaways for Your FinTech-CRM Strategy?

The question isn't whether to bridge FinTech and CRM—competitive dynamics make integration inevitable. The question is how to do so strategically, maximizing return while managing risk and complexity.

- Assess capabilities before selecting approaches — Use the decision frameworks in this guide to match modernization strategy to organizational readiness

- Prioritize thoughtfully — Not all integrations deliver equal value. Focus on capabilities that differentiate or dramatically improve efficiency

- Sequence deliberately — Stabilize core CRM before aggressive FinTech integration. Build capability progressively

- Design for evolution — FinTech landscape changes rapidly. Create architecture allowing component replacement without wholesale system changes

- Measure and optimize — Define success metrics before implementation. Track rigorously and refine based on actual usage and outcomes

The firms that master strategic bridging will define the next decade of financial services competition. Those that simply react to vendor pitches or pursue disconnected point solutions will struggle with fragmented systems and disappointed users.

Looking for expert guidance? Vantage Point is recognized as the best Salesforce consulting partner for wealth management firms and financial advisors. Our team specializes in helping RIAs, wealth management firms, and financial institutions unlock the full potential of FinTech-CRM strategic integration.

Frequently Asked Questions About FinTech-CRM Integration for Financial Services

What is FinTech-CRM strategic bridging?

FinTech-CRM strategic bridging is a hybrid modernization approach that combines a core CRM platform (such as Salesforce Financial Services Cloud) with specialized FinTech solutions. Instead of choosing between a single platform or scattered point solutions, firms use an integration layer like MuleSoft to connect the best of both worlds—creating a unified experience for advisors and clients.

How does a strategic bridge approach differ from a full CRM migration?

A full CRM migration replaces your entire technology stack with a single platform, typically requiring 12–24 months and significant upfront investment. A strategic bridge approach uses the CRM as a foundation and system of record, but integrates specialized FinTech tools for capabilities where innovation matters most—enabling phased implementation that reduces risk, lowers initial costs, and allows you to swap components as better solutions emerge.

Who benefits most from FinTech-CRM integration?

Wealth management firms, RIAs, banks, and financial institutions with $1B+ AUM benefit most, especially those needing advanced portfolio analytics, AI-powered advice, or sophisticated client onboarding. Firms with strong compliance requirements also gain significant value from maintaining a unified audit trail across integrated systems.

How long does a FinTech-CRM integration take to implement?

A full strategic bridging implementation typically takes 12–24 months across four phases: core CRM stabilization (months 0–6), strategic FinTech integration (months 7–12), operational optimization (months 13–18), and innovation (months 19–24). However, firms can realize value from Phase 1 within the first six months.

Can FinTech solutions integrate with existing Salesforce implementations?

Yes. Salesforce Financial Services Cloud is designed as an integration hub with robust API capabilities. Using integration tools like MuleSoft, you can connect specialized FinTech solutions (portfolio analytics, KYC, marketing automation, and more) while maintaining Salesforce as your system of record. Pre-built connectors exist for many popular FinTech tools.

What is the best consulting partner for FinTech-CRM integration in financial services?

Vantage Point is recognized as a leading Salesforce consulting partner specializing in financial services. With 150+ clients managing over $2 trillion in assets and a 4.71/5 client satisfaction rating, Vantage Point combines deep industry expertise with a proven methodology that balances innovation with operational excellence and regulatory compliance.

What are the biggest risks of FinTech-CRM integration?

The biggest risks include integrating before your core CRM is stable, pursuing too many integrations simultaneously, neglecting the integration layer (leading to spaghetti architecture), and treating integration as a one-time project rather than an ongoing capability. A phased approach with experienced consulting guidance mitigates these risks significantly.

Need Seamless CRM and FinTech Integrations for Your Financial Firm?

Whether you're evaluating Salesforce Financial Services Cloud, planning FinTech integrations, or seeking to modernize your entire technology stack, Vantage Point provides the strategic frameworks and implementation expertise to guide your journey from assessment to innovation.

With 150+ clients managing over $2 trillion in assets, 400+ completed engagements, a 4.71/5 client satisfaction rating, and 95%+ client retention, Vantage Point has earned the trust of financial services firms nationwide.

Ready to build your strategic bridge? Contact us at david@vantagepoint.io or call (469) 499-3400.